By Bob Cunneen, Senior Economist and Portfolio Specialist, MLC

“Politics is the art of looking for trouble, finding it everywhere, diagnosing it incorrectly and applying the wrong remedies.”

Groucho Marx

“One of Australia’s most important national assets is our institutional arrangements: things like the rule of law, our strong and credible institutions, and our stable political system.”1

Reserve Bank of Australia Deputy Governor, Dr Philip Lowe, 12 August 2015.

The Winners Curse

Australian investors have been historically blessed with good fortune compared to others. Australian shares have delivered strong returns in terms of capital growth and dividends over the past century. Over the 115 years since 1900, Australia has been the second-best performing equity market with a real return of 7.3% per year.2

For the past 25 years, Australia has seen continuous economic growth and a solid financial system. Australia’s population is growing and the labour force is highly skilled. Australia’s natural resources – iron ore, coal, industrial metals and land – have been key sources of export income. While there has been some sharp setbacks in the recent past – the Asian Financial Crisis (1997-98) and the Global Financial Crisis (2007-09) being notable – Australia has managed to come through these events with remarkable resilience. This past success reflects both individuals and institutions that have proven flexible and policymakers who were agile.

The Leadership revolving door

Yet Australia’s prosperity is now being challenged by increasing political risk. Political risk can come in various forms. These political risks can range from sudden leadership switches and significant policy changes to the more extreme examples of conflict and revolutions that dramatically alter the political order. Fortunately in Australia’s case, we are not considering the dramatic political risk that involves violence. Here the more modest form of political risk in leadership and policy changes are considered. Australia has been prominent in this moderate political risk spectrum.

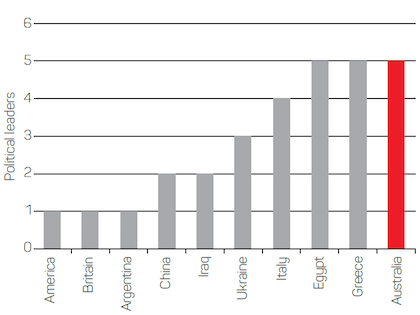

The clearest example of Australia’s political risk is the revolving door of the Prime Minister’s office. For the period 2010 to 2015, Australia had five Prime Ministers in the poetic sequence of: Rudd, Gillard, Rudd, Abbott, Turnbull. Chart 1 shows how Australia rivals Italy and Greece in terms of political turnover at the top.

Considering that both Italy and Greece have struggled over the past decade with stagnating economies and high unemployment, Australia has achieved a remarkable place on this leadership instability podium.

Chart 1: Number of changes to political leadership by country between 2010 and 2015

Source: NAB Asset Management.

With sharper swings in policy uncertainty

Political risk is also evident with the increasing uncertainty over Australia’s economic and regulatory policy. Investors face considerable challenges in assessing the likely policy agenda of governments when the willingness to implement their policy agenda is hostage to opinion polls and media commentators.

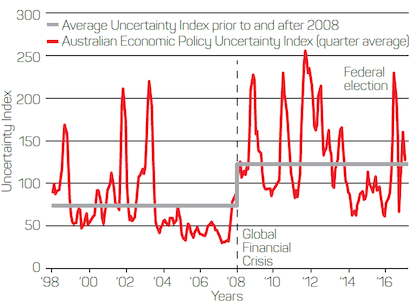

A notable measure of this is the ‘Economic Policy Uncertainty Index’ (EPU) which counts newspaper articles which include words such as “uncertainty”, “economy”, “regulation” and “taxation”.3 Chart 2 shows occasional spikes in the EPU Index for Australia which may be in response to a major global crisis, such as the GFC, or a specific domestic event, such as the federal election which is held in Australia every three years. However the more ominous signal is not these temporary spikes in “uncertainty”, but rather that the average level of the EPU has risen since 2008. This suggests that Australia’s “policy uncertainty” has increased materially.

Should investors worry about this heightened “policy uncertainty”? Yes. A ‘Working Paper’ released by the International Monetary Fund (IMF) looked at 169 countries over the period 1960 to 2004 and found that “higher degrees of political instability are associated with lower growth rates of GDP per capita”.4 This same research also highlighted that political instability affects economic growth “by lowering the rates of productivity growth and, to a smaller degree, physical and human capital accumulation”.

Chart 2: The Economic Policy Uncertainty Index for Australia

Source: Economic Policy Uncertainty, as at 28 February 2017.

But not quite yet Argentina

Argentina is a prime example of how political instability can play havoc with economic prosperity. Argentina has had a “century of decline” relative to other countries according to The Economist.5 Various reasons are given for Argentina’s demise – the “pendulum” of policy changes from intervention to liberalisation, the prevalence of “short-termism” as well as the high dependence on commodity exports. Interestingly, The Economist compared Argentina’s historical woes to Australia’s achievements over the past century and complimented Australia for having “institutions to balance competing interests”. Yet this charitable assessment of Australian politics in 2014 is now difficult to reconcile with the inability to achieve federal budget repair, the focus on opinion polls and the pantomime of Parliament’s question time. Australia is certainly not yet Argentina, but the symptoms of political risk are emerging.

Australia’s political fragility may only become evident over an extended period. Australian asset classes could face the “boiling frog” scenario – when the political temperature becomes progressively warmer until consciousness is completely lost and investment returns become terminal. Australian investors need to consider global diversification given this increasing political risk. Essentially “patriotism is the last refuge of the scoundrel” as well as the prudent investor.6

If you would like to discuss anything in this article, please call us on |PHONE|.

1.National wealth, land values and monetary policy’ speech, Reserve Bank of Australia Deputy Governor, Dr Philip Lowe, 12 August 2015.

2. ‘Credit Suisse global investment returns yearbook 2015’, Credit Suisse, February 2015. Past performance is not a reliable indicator of future performance. The value of an investment may rise or fall with the changes in the market.

3. ‘Economic Policy Uncertainty Index for Australia’, Economic Policy Uncertainty.

4. ‘How does political instability affect economic growth?’, Aisen A and Veiga F, IMF Working Paper, January 2011. Note the views expressed in this Working Paper are those of the authors and do not necessarily represent those of the IMF or IMF policy. Working Papers describe research in progress by the authors and are published to elicit comments and to further debate.

5. ‘A tragedy of Argentina: A century of decline’, The Economist, 17 February 2014.

6. ‘Patriotism is the last refuge of the scoundrel’, Pronouncement, Johnson S (1709-1784).

Important information

This publication is provided by MLC Investments Limited (ABN 30 002 641 661, AFSL 230705) (MLCI) a member of the group of companies comprised National Australia Bank Limited (ABN 12 004 044 937, AFSL 230686), its related companies, associated entities and any officer, employee, agent, adviser or contractor therefore (‘NAB Group’). Any references to “we” include members of the NAB Group. An investment in any product or service referred to in this publication does not represent a deposit or liability of, and is not guaranteed by NAB or any other member of the NAB Group.

This information may constitute general advice. It has been prepared without taking account your objectives, financial situation or needs and because of that you should, before acting on the advice, consider the appropriateness of the advice having regard to your personal objectives, financial situation and needs.

Past performance is not a reliable indicator of future performance. The value of an investment may rise or fall with the changes in the market.

This information is directed to and prepared for Australian residents only.

Any opinions expressed in publication constitute our judgement at the time of issue and are subject to change. Neither MLCI nor any member of the NAB Group, nor their employees or directors give any warranty of accuracy, not accept any responsibility for errors or omissions in this publication.